Managing personal finances can feel overwhelming. This is especially true when juggling multiple expenses, savings goals, and unexpected costs. Fortunately, the 50/30/20 rule provides a simple and effective budgeting strategy that helps you to allocate income efficiently while maintaining financial stability.

Developed by U.S. Senator Elizabeth Warren and outlined in her book All Your Worth: The Ultimate Lifetime Money Plan.

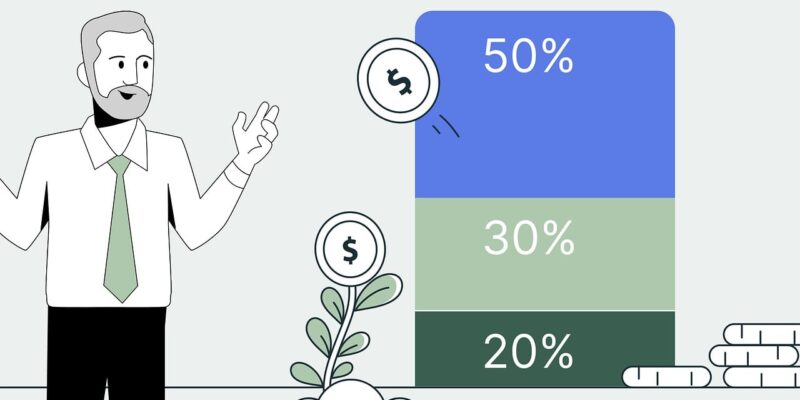

this budgeting method divides after-tax income into three key categories:

50% for Needs (Essential expenses)

30% for Wants (Lifestyle and discretionary spending)

20% for Savings & Debt Repayment

This flexible approach allows you to cover necessities, enjoy life. It also allows you to work toward long-term financial goals without unnecessary stress. In this article, we’ll explore how the 50/30/20 rule works. We will also look at its benefits and how to use it effectively. Finally we will cover ways to adjust it for different financial situations.

1. Understanding the 50/30/20 Budget Rule

The 50/30/20 rule is designed to create balance and financial security while simplifying budgeting. It helps you to focus on expenses, reduce debt, and build savings without tracking every penny.

A. Breaking Down the 50/30/20 Rule

🔹 50% – Needs (Essential Expenses) :

This category covers basic living expenses that you need to maintain financial stability.

Rent or mortgage payments

Utilities (electricity, water, gas, internet)

Groceries

Health insurance

Car payments or public transportation

Minimum debt payments

Childcare or education costs

💡 Tip:

If your needs exceed 50% of your income, look for ways to cut costs. You may have to refinance loans, negotiate bills, or reduce discretionary expenses.

🔹 30% – Wants (Lifestyle & Discretionary Spending) :

The wants category includes non-essential expenses that enhance your lifestyle and bring enjoyment.

Dining out, takeout, and coffee runs

Entertainment (movies, concerts, streaming subscriptions)

Gym memberships and hobbies

Shopping (clothes, electronics, luxury items)

Travel and vacations

💡 Tip:

If you’re saving for a big goal, consider reducing spending in this category. Extra funds can be reallocated towards the needs category.

🔹 20% – Savings & Debt Repayment The final 20% is allocated toward building financial security and reducing debt.

Emergency fund savings

Retirement contributions (401(k), IRA)

Investing (stocks, bonds, real estate)

Extra debt payments (credit cards, student loans, car loans)

💡 Tip:

Automate savings contributions. You can do this by setting up direct deposits into a separate account to make saving effortless.

2. Benefits of the 50/30/20 Budget Rule

The simplicity of the 50/30/20 rule makes it an excellent budgeting approach for beginners. It is also useful for those looking for a structured yet flexible financial plan.

1. Easy to Follow and Implement

Unlike complex budgeting spreadsheets, this rule simplifies money management into three straightforward categories.

2. Encourages Balanced Spending

By allocating money for both needs and wants, this method prevents over-saving or excessive spending, promoting financial stability and enjoyment.

3. Helps You Achieve Financial Goals Faster

By prioritizing savings and debt repayment, you can build wealth, reduce financial stress, and prepare for the future.

4. Reduces Decision Fatigue

This budgeting method eliminates the need for micromanaging expenses, making it easier to stay on track.

5. Adaptable to Different Income Levels

The 50/30/20 rule works for various income brackets and can be adjusted based on personal financial situations.

3. How to Apply the 50/30/20 Rule to Your Finances

Step 1: Calculate Your After-Tax Income

To determine your budget allocations, start by calculating your monthly take-home pay (after taxes and deductions).

✔ Example: If you earn $4,000 per month after taxes:

Needs (50%) = $2,000

Wants (30%) = $1,200

Savings & Debt Repayment (20%) = $800

💡 Tip: If you have irregular income (freelancers, gig workers), calculate an average monthly income based on past earnings.

Step 2: Identify and Categorize Your Expenses

Review your bank statements and spending habits to categorize expenses. Separate them into Needs, Wants, and Savings/Debt Repayment.

✔ Use budgeting tools/apps like:

Mint

YNAB (You Need a Budget)

EveryDollar

Personal Capital

💡 Tip: Track expenses for one month to get a clear picture of spending habits.

Step 3: Adjust and Optimize Your Spending

If your spending doesn’t align with the 50/30/20 allocation, consider making adjustments:

✔ If Needs exceed 50%: Reduce fixed expenses (downsize housing, lower utility bills, cook at home). ✔ If Wants exceed 30%: Cut back on luxury purchases, dining out, or subscription services. ✔ If Savings is below 20%: Automate transfers to a savings account and prioritize debt payments.

💡 Tip: Use the “pay yourself first” method by transferring savings before spending on wants.

4. Adapting the 50/30/20 Rule for Different Financial Situations

The traditional 50/30/20 rule is a great starting point. However, please note it can be adjusted based on your income level, debt obligations, and savings goals.

A. High-Income Earners

✔ Recommended Adjustments:

Increase savings percentage (30-40%) for retirement or investments.

Reduce discretionary spending and prioritize wealth-building.

B. Low-Income Earners or High-Debt Individuals

✔ Recommended Adjustments:

Shift to 60/20/20 (60% Needs, 20% Wants, 20% Savings).

Focus on reducing debt and building an emergency fund first.

Consider side hustles or extra income streams.

C. Students or Young Professionals

✔ Recommended Adjustments:

If debt is high, allocate more to repayment (e.g., 40% Needs, 20% Wants, 40% Savings/Debt).

Build an emergency fund before investing.

D. Families with Children

✔ Recommended Adjustments:

Increase savings for education funds (e.g., 529 college savings plans).

Reduce unnecessary lifestyle expenses to accommodate family needs.

5. Common Mistakes to Avoid When Using the 50/30/20 Rule

1. Underestimating Needs vs. Wants Many people misclassify expenses—for example, upgrading a phone is a want, not a need.

2. Not Adjusting the Budget as Income Changes Life circumstances change! Reevaluate your budget quarterly to stay aligned with financial goals.

3. Ignoring Debt Payments If you have high-interest debt. Always focus on paying it off faster rather than sticking strictly to 20% savings.

4. Not Tracking Expenses Regularly. monitor spending to ensure you stay within your budget allocation.

5. Failing to Build an Emergency Fund. Always allocate savings for unexpected expenses, so you don’t rely on credit cards or loans.

Make the 50/30/20 Rule Work for You

The 50/30/20 rule is an easy, flexible, and effective budgeting method that simplifies money management. It helps to keep your finances balanced. Whether you’re a beginner looking for structure or a seasoned budgeter seeking efficiency. This method provides a roadmap to financial success.

Take Action Today:

- ✅ Calculate your after-tax income.

- ✅ Categorize your expenses into Needs, Wants, and Savings.

- ✅ Adjust your spending to align with the 50/30/20 rule.

- ✅ Monitor and refine your budget regularly.

A financially secure future starts with smart money management today—and the 50/30/20 rule makes it easy to get there! 💰🚀

References

Warren, Elizabeth. All Your Worth: The Ultimate Lifetime Money Plan. Free Press, 2005.

U.S. News & World Report. “Budgeting Strategies That Actually Work.” www.usnews.com

NerdWallet. “50/30/20 Budget Rule Explained.” www.nerdwallet.com

Investopedia. “How to Budget Your Money with the 50/30/20 Rule.” www.investopedia.com

Consumer Financial Protection Bureau (CFPB). “Managing Your Finances Wisely.” www.consumerfinance.gov

Comments